The P4 Framework

Written by: Andrew Siwo

Edited by: Adam Terragnoli

This article intends to serve as a guide and resource for asset owners and managers investing in or managing impact investment strategies. Moreover, the article describes the ‘P4 Framework,’ a practical tool for assessing the opportunity set of impact investment managers.

“Impact investing” has entered its second decade. This investment approach has the dual objective of achieving a financial return and generating a social and/or environmental benefit. Such benefits can include anything from addressing affordable housing to mitigating climate change, depending on the mandate of the investment manager.

How does an investor assess the capability of an impact investment strategy to deliver on its mandate? The International Finance Commission (“IFC”) has developed Operating Principles for Impact Management[1] that are guidelines of what should be expected from an impact investment. As of this publication, no universal standard exists to assess impact across standard demographics (geographies, asset classes, and sectors) and financial return expectations. So then how does an investor assess an impact investment strategy’s ability to perform optimally? Investors are not able to reliably do so and so many hold the view that is not much distinction between the quality of impact managers partly because of the inability to simultaneously and reliably measure both impact and return.

The Global Impact Investing Network (“GIIN”) produces an annual survey to capture the assets under management and planned activity of impact funds globally. The most recent GIIN survey reported[2] that globally managed impact assets have reached an estimated $502 billion — more than a 50-time increase from the $10 billion figure reported in its 2013 survey.[3] On the surface, this figure seems to suggest rapid growth. However, because the characteristics that define impact investments are somewhat nebulous, there remains doubt on the accuracy of this $502 billion figure. In many cases, funds that invest in companies with a strong focus on environmental, social, and governance (“ESG”) concerns, representing a total of $12 trillion, consider their activity sufficient to be marketed as impact investing. Moreover, according to GIIN’s 2019 annual survey, some of the 1,340 survey respondents felt that “everything they do is impact investing,” which alone raises some major concerns of impact legitimacy as well as the consistent application and agreement to the qualifications of an impact investment.

It is not surprising that the absence of stringently followed or applied definitions has fueled the proliferation of impact investment vehicles. As more capital is driven towards the impact space, new general partners that were on the sidelines have begun to take notice and act opportunistically. As a result, it should be clear that asset growth for impact-oriented investment managers should not be readily accepted as the sole criterion for measuring the success (or even growth) of legitimate impact investments.

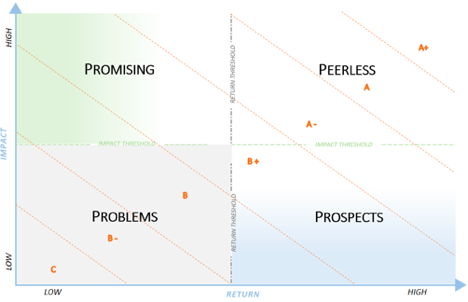

The P4 Framework addresses the challenge of impact investment valuation by assigning a grade based on an investment’s ability to achieve its definitional mandate—i.e., financial return and impact. Although the grades reward strategies that can achieve the highest level of return and impact, not all impact sectors offer market-rate solutions (i.e., achieve high returns). Similarly, high impact cannot be achieved in all sectors. Take, for example, an impact fund with the goal of creating jobs in Beverly Hills, California, versus a strategy seeking to create jobs in Kampala, Uganda. Many would argue that job creation in an emerging market benefitting a vulnerable population is highly impactful, whereas the same activity elsewhere is generally less impactful. The P4 Framework assigns a grade across the four cross-sections of impact – “Peerless,” “Promising,” “Problems,” and “Prospects.” Most opportunities are either “Promising” (low return/high impact) or “Prospects” (high return/low impact). Investments that are “Peerless” are those that can achieve a high return and high impact; those that are “Problems” generate a low return and low impact. The framework helps plot how an impact manager ranks in relation to impact and return. Financial performance benchmarks are useful in determining the return expectation of a particular fund. Impact, although much more nebulous, can be measured by the degree in which capital deployment provides positive social or environmental benefits that otherwise would not have occurred.

The next phase of impact investing will have a larger sample size of investment funds to better assess managers on the dual objective of their strategies. In the earliest impact funds, many professionals involved often lacked the relevant investment experience and financial acumen; these initial impact investors were commonly, and sometimes disparagingly, viewed as “tree huggers” by traditional asset managers. Peter Lupoff, who taught impact investing at Fordham University and manages his family office’s impact portfolio, more generously describes earlier impact managers as “steeped in the social/environmental challenges but light on traditional asset-management skills.” Further, “impact investing is on the rise, and it is imperative that practitioners effectively educate and align the next generation of asset owners and managers to ensure a viable future for the space.”

The P4 Framework is a tool intended to better compartmentalize the various options available for impact investing in fostering the transparency necessary to identify strategies based on the relative objectives of investors. The framework captures the fundamental qualities of impact investments across both impact and return objectives. As impact investing grows and matures, the return capabilities of various impact sectors will become clearer, which will signal to investors and investment managers how to best allocate capital. Impact investing can benefit from tools like the P4 Framework, which can aid the successful development and continued growth of the space by enhancing the credibility of impact investment valuation.

References

- “What Is Impact Investing?” Operating Principles for Impact Management. World Bank Group . Accessed November 4, 2019. https://www.impactprinciples.org/ ↑

- “Global Impact Investing Market Soars above $500bn.” Global impact investing market soars above $500bn | The Social Enterprise Magazine – Pioneers Post, October 31, 2018. https://www.pioneerspost.com/news-views/20190401/global-impact-investing-market-soars-above-500bn. ↑

- Perspectives on Progress: The Impact Investor Survey, (2013), J.P. Morgan https://thegiin.org/assets/documents/Perspectives%20on%20Progress2.pdf ↑